CÔNG TY CỔ PHẦN ĐẦU TƯ NAM LONG (HOSE: NLG)

Số 6 Nguyễn Khắc Viện, P. Tân Phú, Quận 7, TP.HCM

Điện thoại: (84.28) 54 16 17 18

Fax: (84.28) 54 17 18 19

20/09/2018

One day in July, Ms. Nguyen Mai Phuong, a 45-year-old businesswoman living in Ho Chi Minh City’s Binh Thanh district, visited a few banks to seek a loan of VND2.5 billion ($110,000) to purchase land. She was told of the new interest rates on home loans, ranging from 8-10 per cent per annum for the first year, depending on the customer’s objectives, and then 11-12 per cent. “I’m re-considering my plans, as these rates are much higher than a few months ago,” she said.

Most local real estate developers have also been restricted in approaching capital resources over the last year due to the State Bank of Vietnam (SBV)’s moves to tighten capital flows into the local property market by raising the credit risk on real estate loans and reducing the proportion of short-term capital to be used for medium- and long-term loans by commercial banks, due to concerns about bad debts amid the land price “fever” in the country.

Accordingly, banks have raised rates on property mortgages by 1-2 percentage points over the last few months, with lending rates rising to 12 per cent for mid-term loans and 12.5 per cent for long-term loans. “Such steps are aimed at market stability per a specific roadmap after a long time of strong development, and have been a test for real estate developers that overly depend on bank credit but which will help purge the local market,” said Ms. Pham Ngoc Thien Thanh, Research and Consulting Manager at CBRE Vietnam.

Total outstanding loans in real estate and consumer lending have increased sharply in recent times, making it necessary to limit consumer loans being used for investment in the real estate sector. The sector has been booming for some time, leading to a rapid surge in land prices in areas poised to become special administrative - economic zones, according to the Vietnam Real Estate Association (VNREA).

Figures from the SBV show that outstanding loans in the first half of 2018 rose 6.16 per cent compared with the end of last year. Consumer lending grew 6.86 per cent and real estate loans by just 2.19 per cent; significantly down on 2017. Credit growth was reported at 8.56 per cent last year compared to 12.86 per cent in 2016. At the same time, loans for real estate investment and business activities reached $20.2 billion, accounting for 6.5 per cent of the total, down from 7.7 per cent in 2016.

The central bank has adopted measures since earlier this year to exert strict control over credit in real estate by way of limiting loans to no more than 70 per cent of a property’s value instead of the previous 80-90 per cent. It attributes the measures to concerns over market risk, with the real estate credit risk jumping from 150 per cent to 250 per cent in the past few months. In Circular No. 19 issued late last year, the SBV put forth a target of reducing the use of short-term deposits for mid- and long-term loans in 2018 and 2019 to 45 per cent and 40 per cent, respectively, instead of the previous 60 per cent.

Having learned a number of lessons from the real estate bubble and downturn in the 2008-2013 period, the SBV has set its sights on 17 per cent credit growth this year and has requested credit institutions closely monitor growth by limiting loans for property and stocks and supervising consumer loan borrowers who actually invest in real estate and securities. “Along with interest rate increases, some banks have tightened their cash flows to real estate by cutting preferential loans, pushing up interest rates on pre-payments, and setting stricter conditions for borrowers, which makes developers and homebuyers face more difficulties in accessing loans,” said Mr. Huynh Ba Lan, Chairman of the Kien A JSC.

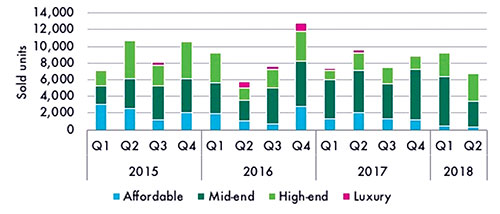

HCMC apartment sales, by segment, 2015-Q2 2018

[Source: SBV, 2018]

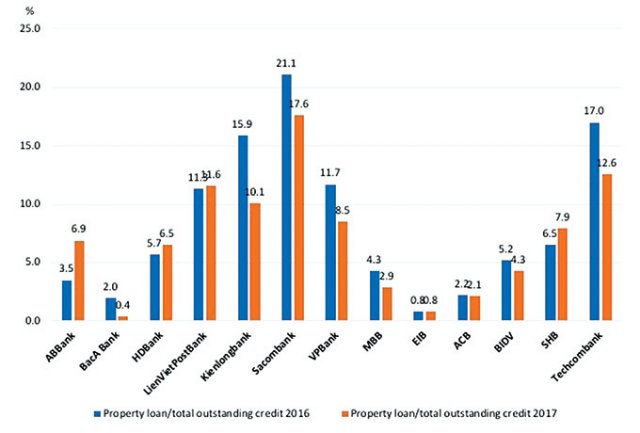

Proportion of local bank real estate loans, 2016-2017

[Source: SBV, 2018]

A host of SBV credit tightening strategies along with solid macroeconomic fundamentals continued to create momentum for Vietnam’s real estate market to develop stably in the first half of 2018. The housing market continues to witness steady growth. In major cities like Hanoi and Ho Chi Minh City, sales volumes have remained the same in the first half of the last three years, at 14,000-15,000 units. In terms of price, the primary sale price in Hanoi has not changed much, at $1,130 per sq m, while in Ho Chi Minh City in the second quarter it stood at $1,580 sq m, up 3 per cent quarter-on-quarter, thanks to a number of luxury projects with favorable locations opening, according to CBRE Vietnam.

Mr. Le Hoang Chau, Chairman of the Ho Chi Minh City Real Estate Association (HoREA), said property credit in the city stood at over 30 per cent of the total ten years ago but has been around 10 per cent for the last three years. The central bank frequently issues directions asking banks to strictly follow its warnings and only issue loans to investors with the financial capacity to repay. The rate of bad debts in real estate loans is therefore only 2-2.5 per cent in the city, he said.

Its real estate market showed signs of “cooling down” in the first half of this year compared to 2017, in terms of both new supply and sales in almost all segments, according to DKRA Vietnam. “The local market has self-adjusted and remained stable,” said Mr. Nguyen Hoang, R&D Director at DKRA Vietnam. “In the second half of this year the city continues to maintain stable development, meaning that new supply will be adjusted against the consumption rate.”

Similarly, Mr. Cameron Joyce, Research Manager at Viet Capital Securities (VCSC), said changes and proactive macro-prudential measures should help dampen any potential extremes in the current real estate cycle while reducing the probability of another crisis. They will certainly have some moderate cooling effect on market. Even though the market continues in an uptrend, with moderate price gains in the affordable and mid-range segments, transaction volumes remain stable. In the event of a cyclical slowdown, he said, this also means that the government has some dry powder available should it wish to provide support to the sector.

The gradual reduction in reliance on bank credit has not only been a challenge but also an opportunity for enterprises to restructure, with capital aimed at growing businesses and making the local real estate market more transparent, healthy and sustainable, Mr. Chau said. Meanwhile, according to Mr. Nguyen Minh Quang, Director of the Sales & Marketing Division at the Nam Long Corporation (NLG), the SBV’s credit restrictions have not hindered the corporation’s ability to mobilize capital.

As at the end of the second quarter, NLG had short-term and long-term loans of around $45 million, while its debt-to-equity ratio is 0.23, significantly reducing its dependence on debt. “We have been assessed by the Ho Chi Minh City Securities Company (HSC) as being one of only a few property developers with low debt ratios and are less affected by interest rate fluctuations,” Mr. Quang said. “We can be active in capital resources to expand our land reserves and build projects without too much dependence on loans.”

Over the past two years, NLG has announced strategic partnerships with Japanese investors in a number of major projects in Ho Chi Minh City, to gain support in terms of both financing and experience. “Foreign investors have been active in identifying investment projects in Vietnam, while local developers usually need capital,” Mr. Quang explained. “Cooperation between local and foreign investors is therefore now quite common. But persuading international investors has always been a major challenge for local businesses, with a sound vision, long-term plans, governance capacity, transparency, and commitment to performance being key factors in success.”

Meanwhile, apart from investing in real estate, local developer Kien A has also made investments in other sectors, including finance, trading, imports-exports, and construction. “Our business diversification has helped us maintain capital resources, balance our finances, and have safe capital flows for the real estate business, in which we can ensure construction schedule and quality,” Mr. Lan said.

Many local investors over recent years have actively diversified their capital resources under cooperation deals and merger and acquisitions (M&As) at home and abroad, loans from customers, bank loans, and capital from listing on the stock market, according to Mr. Hoang from DKRA. Figures released at an M&A seminar in early August in Ho Chi Minh City showed that the real estate sector ranked first with 66.75 per cent of M&A deals in the first half this year, followed by banking and finance and industrial manufacturing.

Mr. Quang also revealed that NLG will continue to invest in a new land fund, expand development, increase its market share, and strengthen its advantages in matters foreign investors are concerned about in order to seek further investment opportunities. To secure sustainable growth, he recommended Vietnamese developers have a strategic vision and orientation for long-term development, enhance the foundations for creating products in the market, ensure a financial balance, and enhance their ability to cope with market fluctuations or sudden change.

From Vneconomictimes.

16/01/2024

The lively look of Mizuki Park TownshipCÔNG TY CỔ PHẦN ĐẦU TƯ NAM LONG (HOSE: NLG)

Số 6 Nguyễn Khắc Viện, P. Tân Phú, Quận 7, TP.HCM

Điện thoại: (84.28) 54 16 17 18

Fax: (84.28) 54 17 18 19

CÔNG TY CỔ PHẦN ĐẦU TƯ NAM LONG (HOSE: NLG)

Số 6 Nguyễn Khắc Viện, P. Tân Phú, Quận 7, TP.HCM

Điện thoại: (84.28) 54 16 17 18

Fax: (84.28) 54 17 18 19